GS Paper III

News Excerpt:

Javier Milei, the recent winner of Argentina’s presidential election, has drawn attention for his unconventional policies, including replacing the country’s peso currency with the dollar.

What is Dollarisation?

Dollarisation refers to using the U.S. dollar in addition to or of another country's indigenous currency. It represents currency substitution.

- When a country's own currency loses its utility as a medium of exchange owing to hyperinflation or instability, it is said to have dollarised.

Why do countries shift to Dollarisation?

- Dollarisation is common in developing nations with weak central monetary authority or unstable economies. It can be an official monetary policy or a de facto market process. The United States dollar comes to be recognised as a generally accepted medium of exchange for use in day-to-day transactions in a country's economy, either through official decree or through acceptance by market participants.

- The primary reason for dollarisation is better currency value stability over a country's indigenous currency.

-

- For example, the inhabitants of a country in an economy experiencing rampant inflation may prefer to conduct day-to-day transactions in the United States dollar because inflation will lower the purchasing value of their own currency.

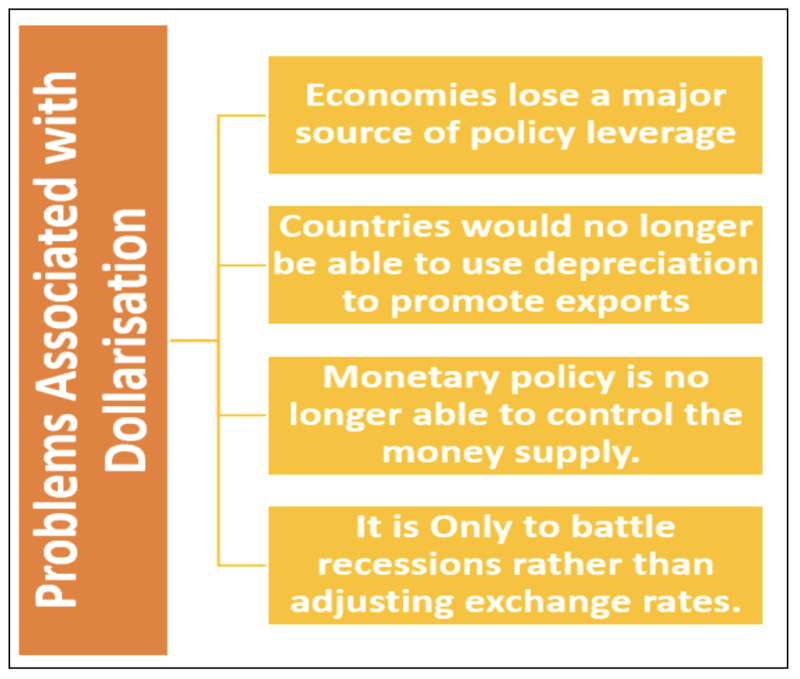

- By modifying its money supply, the government gives up some of its potential to affect its own economy through monetary policy. The dollarising country outsources its monetary policy to the Federal Reserve of the United States.

Is dollarisation a solution to an economy?

- Dollarisation can help control hyperinflation by breaking the vicious cycle between price rises and rising money supply.

- If the domestic currency is replaced by dollars, the money supply can no longer be controlled by vested political interests that can raise spending for political purposes.

- Prices would be forced to moderate because customers would no longer be able to access currency, decreasing consumption demand conveniently.

- Dollarisation can also be beneficial to growth.

-

- Because a tiny economy can only access dollars through international trade and/or capital inflows, it would incentivise the economy to focus on export achievements while easing conditions for foreign capital, which would be more eager to participate in a stable currency economy.

- The dollar's constant value would ensure that foreign and domestic economic agents could make long-term plans for economic activity, which would otherwise be impossible with a currency that rapidly lost value.

Countries Adopted Dollarisation (CASE STUDY):

Three fully dollarised economies — Ecuador, Panama, and El Salvador — have had successful economic outcomes following dollarisation, with Ecuador being a helpful case study.

- Reasons: The Ecuadorian economy suffered a series of debilitating crises in the late 1990s, with economic output contracting by almost 7%, inflation at roughly 67%, and the domestic currency, the Sucre, depreciating by almost 200% in 1999. President Jamil Mahuad announced the adoption of the dollar in January 2000; widespread protests following the move forced him to resign two weeks after the announcement. Despite this political upheaval, Ecuador persisted with dollarisation. The inflation rate in Ecuador hit a high of 108% in September 2000.

- Progress shown by Ecuador After Dollarisation: The economy has shown considerable progress on parameters measuring economic growth and social welfare. The World Bank estimates a growth of 4.5% in real GDP between 2001 to 2014. The poverty rate fell from 36.7% in 2007 to 22.5% in 2014, with inequality, as measured by the Gini index, falling by 9 percentage points over this period. During the 2008 recession, the economy lost only 1.3% of GDP, reaching its 20-year growth trend only two years after the onset of the recession. Following dollarisation, the inflation rate averaged around 4% between 2003 and 2006, a remarkable achievement for an economy experiencing double-digit inflation rates since the 1970s. The foreign debt to GDP ratio also reduced from 55% in 2000 to 21.5% in 2006.

- The adoption of the euro fuelled growth in Greece, with capital inflows rising and tourism booming on the back of a stable currency.

-

- However, in the wake of the Eurozone crisis, Greece was bereft of fiscal and monetary policy space, with monetary policy being determined by the European Central Bank (ECB) and fiscal policy being restrained as a pre-condition for adopting the Euro.

- Zimbabwe conducted a dollarisation experiment to explore if using foreign currency could reduce inflation and stabilise the economy. In July 2008, Zimbabwean dollar inflation was reported to be 2.2 million per cent.

- According to the acting finance minister, a limited number of merchandisers and shops would accept the US dollar as legal tender. Following the experiment, the finance minister declared that the government would adopt the US dollar, legalising its widespread usage in 2009 and suspending the Zimbabwe dollar in 2015.

Way Forward:

Dollarisation may have broken the back of inflation, but active fiscal policy played an important role in ensuring sustainable growth. Several economists have decried a return to austerity economics in Ecuador, with the International Monetary Fund (IMF) insisting on the independence of the Central Bank as a pre-condition for receiving financial assistance. Dollarisation is not a silver bullet; if used well with nimble domestic policy, it can offer a route to success.