Stocktaking on the fintech revolution

Relevance: GS Paper III

Why in News?

The editorial explores the potential and challenges of financial technology (fintech) in India in comparison to the current financial system. It argues for a shift in financial and economic policies to empower fintech to realize its full potential in catering to the diverse requirements of the Indian economy.

|

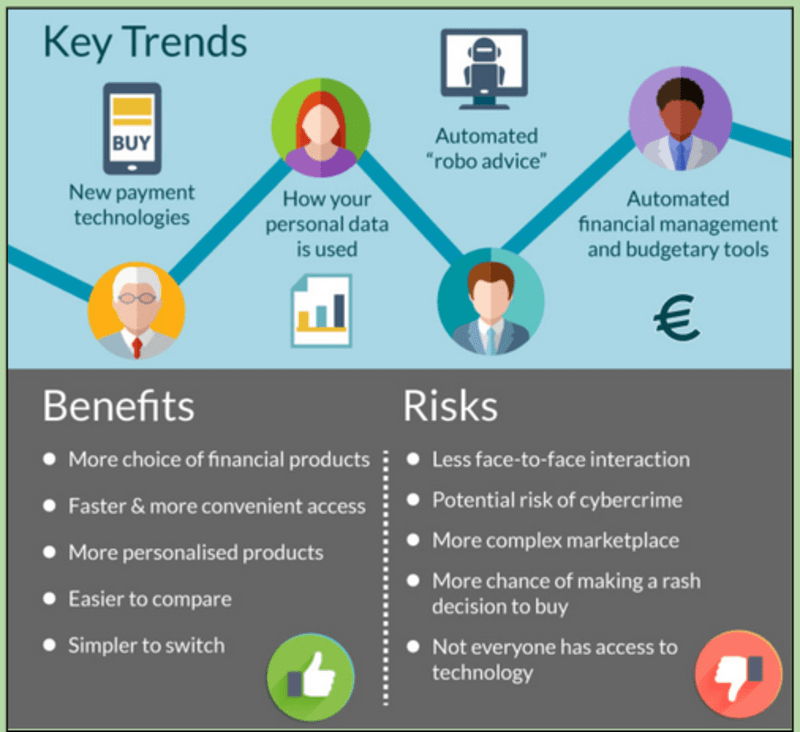

Beyond Editorial: What is Fintech?

Fintech sector in India:

Growth drivers of Fintech:

Way forward:

|

Infirmity of the current financial system:

- Financial economic policy is organised as a central planning system where products, processes, and government-controlled monopolies are imposed from the top.

- It is characterized by bureaucratic, banking and state control of products and processes, which hinders the process of discovery and innovation.

- Further, state control is deepened through government-controlled monopoly systems.

- Limitations in the rule of law make financial firms cautious about innovating.

- The uniquely Indian-style know your customer (KYC) and Prevention of Money Laundering Act restricts the firms.

- The incumbent financial system has weaknesses and is not adapting to the diverse needs of the country's population.

Fintech Revolution:

- The fintech revolution, which aims to replace traditional banking with technology-driven firms, has been a positive development for India, mainly because -

- Banking is a source of systemic risk in India, and a smaller banking system improves stability.

- The incumbent banks are weak in innovating and serving users, so the financial system better serves the real economy when more finance is done without banks in the loop.

- Fintechs can play a crucial role in India, as innovation and risk-taking are required to experiment with many new business models and process designs that can better serve the people.

- For example, mobile phone companies and technology giants like Google can readily make payments, a business that was once a preserve of banking.

Challenges faced by fintech:

- Government protectionism towards traditional banks:

- The levers of the central planning system were used to block competition from new kinds of firms. Policymakers chose to defend banks; they wanted -

- Fintech companies to be service providers to banks

- The main business and profit to be with banks.

- The terms “innovation”, “risk-taking”, and “failure” do not sit well with bankers and the authorities.

- Regulatory hurdles:

- The rule of law provides for checks and balances on the discretionary power of launching an investigation or a prosecution. Most of these guard rails work poorly, making the firms vulnerable and submissive.

- Constraints imposed by the central planning system:

- The government and its agencies specify much about the products and processes. In many aspects, prices are also controlled, making the job of each financial firm a division of a big public-sector system where the basic decisions come from above.

- The central planning system can disrupt a successful business model, or a national champion can come up and eject all private firms.

Conclusion:

Finance is the most important of all industries. It is “the brain of the economy”. The fintech revolution can do a lot for India. But this requires changing the present arrangement of financial economic policy. The future of Indian finance lies in reorienting financial economic policy.